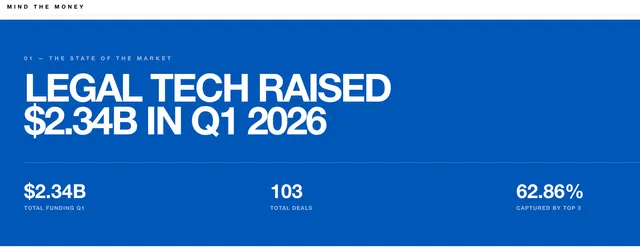

There is a ton of money in LegalTech and that is an awesome headline. Three companies took 63 cents of every dollar raised. The median deal outside those three was a million dollars — seed money, not a growth round. The headline describes a market doing aggressive selection, not broad growth.

The second thing is harder to explain. Legal tech didn't just concentrate this quarter. It split. The trackers lumped together two businesses that share a name and almost nothing else. Legal tech became two businesses this quarter.

The first fork is software platforms selling into law firms. Five companies are pulling away. Three legacy incumbents:, Thomson Reuters, LexisNexis want to own the workflow substrate the industry runs on. Two AI-native insurgents — Harvey and Legora, are turning valuation into revenue faster than anything the category has seen. Harvey: seed to $11B in 3.3 years. All five sell into law firms—the same buyer the category has had for 30 years.

The second fork is harder to see. Lawhive raised a $60M Series B (consumer law, UK). Orbital raised a $60M Series B (real estate, UK). Bretton AI raised ~$70M as a Q1 entrant. All three got categorized as "legal tech." None of them sell software. They use AI to deliver legal services. The unit of delivery is the firm itself. In Q1 2026, this category raised $130M. In all of 2025, $25M. The category established itself in a single quarter.

Fork A and Fork B share a name and almost nothing else. The buyers are different — managing partners and GCs on one side, the end clients those firms used to serve on the other. The competitors are different — other software vendors versus traditional law firms with different regulatory regimes and cost structures. The moats are different — workflow integration versus regulatory authorization to practice. So are the exits: PE and software consolidators versus professional services acquirers who understand what a law firm's unit economics actually look like.

Calling them both "legal tech" is technically correct and analytically useless.

For in-house teams, the fork changes the question. When the category was one thing, you were asking which platform fits your workflow. That question still applies to Fork A. Fork B is a different conversation entirely. If an AI-native firm can deliver the work my outside counsel delivers — at a fraction of the cost, with measurable outcomes, with regulatory authorization to practice — that's a sourcing question, not a vendor question.

Most in-house teams aren't there yet. The AI-native firms cluster in consumer law, real estate, immigration. They haven't moved into commercial work yet.

The headline said "legal tech raised $2.34 billion." The data said "legal tech became two things."

Vist mindthemoney.kenpriore.ai for the numbers